Understanding Overnight Funding on Spot Energies

Why the funding entry on your account can sometimes look larger than you might expect — and what it actually costs you.

The key point

The overnight funding entry you see on your ledger has two parts. Only one of them is an actual cost to you. The other part is a market adjustment that is offset by a corresponding movement in the spot price itself. When market conditions cause a large difference between futures contracts, this adjustment can make up the majority of the funding entry — even though it does not represent a net cost.

How spot energy prices work

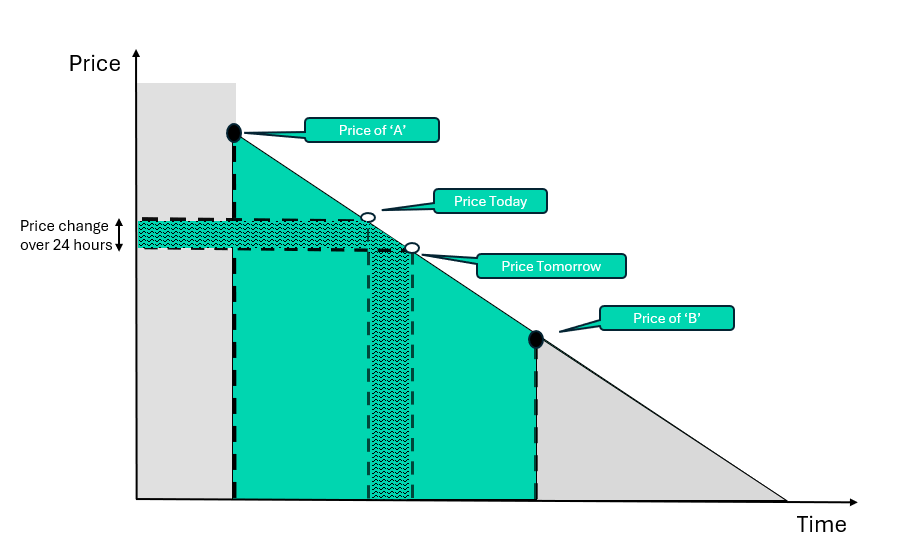

Our spot energy prices (such as Spot Brent Crude) are not taken directly from a single live market. Instead, they are calculated from the two nearest futures contracts — the one closest to expiry (the "near" contract, labelled 'A' in the diagram below) and the one after it (the "next" contract, labelled 'B').

We use a weighted average of these two contracts to create the spot price. As the near contract approaches its expiry date, its influence on the spot price gradually decreases and the next contract's influence gradually increases. This creates a smooth transition rather than a sudden jump in price.

As the diagram shows, the spot price moves slightly each day as part of this transition — even if the underlying market is otherwise flat. The "price change over 24 hours" shown on the left of the diagram represents this daily drift caused by the roll.

When the near contract ('A') is priced higher than the next contract ('B'), the spot price will drift lower day by day. When the near contract is lower, the spot price will drift higher.

What makes up your overnight funding?

The funding entry applied to your account each night has two separate components:

Part 1: Daily basis adjustment

This reflects the daily price movement in the spot market caused by the shifting weighting between the two futures contracts. It is a response to market conditions — similar to how a dividend adjustment works on an index — rather than a charge. It corresponds to a matching movement in your position's running profit or loss.

Part 2: Spreadex charge

This is an annual rate of 3.5%, applied daily. This is the only actual cost of holding your position overnight.

Why does this matter?

The daily basis adjustment and the corresponding spot price movement are designed to broadly offset each other. One appears on your ledger as a funding entry; the other appears in your running profit or loss. The net effect is close to zero. The only genuine cost you bear is the Spreadex charge of 3.5% per year.

Why the funding entry can look larger than usual

When there is a large price difference between the near and next futures contracts, the daily basis adjustment also becomes larger. This can happen during periods of market uncertainty or supply disruption, when near-term prices may move sharply away from longer-term prices.

In these conditions, your ledger may show what appears to be a large overnight funding debit or credit. However, a significant portion of that figure is the basis adjustment — which is offset by the corresponding price movement in the spot market.

Example breakdown

To illustrate how the funding entry breaks down, here is a hypothetical example based on a £1/point position in Spot Brent Crude:

|

Component |

Amount |

What it means |

|

Daily basis adjustment |

£25.00 |

Offset by the corresponding movement in the spot price |

|

Spreadex charge |

£1.00 |

Your actual cost for holding overnight |

|

Total funding entry |

£26.00 |

In this example, the vast majority of the funding entry is the basis adjustment, which is offset by the movement in the spot price. The actual cost to you is £1.00.

Worked example

Suppose the near contract is trading 90 points above the next contract, and there are 3 days until the near contract expires. The spot price will drift approximately 30 points lower per day as the weighting shifts from one contract to the other.

Holding a £1/point short position in Spot Brent Crude overnight:

|

Amount |

|

|

Spot price movement (downward drift from roll) |

+£30.00 profit on position |

|

Daily basis adjustment (funding entry) |

−£30.00 debit |

|

Spreadex charge (3.5% annual rate) |

−£1.00 debit |

|

Your actual cost of holding overnight |

£1.00 |

The £30 basis adjustment and the £30 price movement cancel each other out. What you're left with is the Spreadex charge only.

Note for long positions: the same logic applies in reverse. If the spot price drifts lower, a long position holder sees a loss on the price movement but receives a credit via the basis adjustment. The two broadly offset, and the net cost is again just the Spreadex charge.

Weekend funding (Friday nights)

Funding applied on a Friday night covers three calendar days (Friday, Saturday and Sunday) rather than one. This means both the basis adjustment and the Spreadex charge will be three times the usual daily amount. The same principle applies — the basis adjustment portion is still offset by the corresponding spot price movement, and the only actual cost is three days' worth of the Spreadex charge.

At a glance

|

What you see |

What it means |

|

A large funding debit or credit on your ledger |

Includes the daily basis adjustment — which is offset by the spot price movement |

|

The daily basis adjustment |

Reflects the roll between futures contracts; a market adjustment, not a charge |

|

The Spreadex charge (3.5% p.a.) |

Your only actual cost for holding overnight |

Common questions

Why was I charged more than usual last night?

When there is a large difference between the two futures contracts used to price the spot market, the daily basis adjustment increases. This makes the overall funding entry appear larger. However, the larger basis adjustment is matched by a larger corresponding movement in the spot price, so the net cost to you remains the Spreadex charge of 3.5% per annum.

Is the basis adjustment an extra charge?

No. The basis adjustment is a response to market conditions rather than a charge. It reflects the natural movement of the spot price caused by the roll between futures contracts, and is offset by the corresponding movement in your position's running profit or loss. The only aspect of the overnight funding that constitutes a charge is the Spreadex fee of 3.5% per annum.

Does this apply to all spot commodity markets?

This pricing method and funding structure applies to spot energy markets and spot soft commodity markets (such as coffee, sugar, cocoa and cotton). Spot gold and spot silver are priced differently and have a separate funding arrangement — please refer to our Commodities Market Information page for details on those markets.