Commodities - Market Information

Use the table below to find out all you need to know about spread betting on commodities with Spreadex.

Use the tab sections to access the market information you require for each product or click on the product name to find a full description of the product.

See further below for our Commodities FAQs.

| Product | Trading Hours^ | Trade Per | Spread Width From*** |

|---|---|---|---|

| Commodities, Dailies | |||

| Spot, Brent Crude | 0100-2300 |

1 | 2.8 |

| Spot, Cocoa (London) | 0930-1650 |

1 | 3 |

| Spot, Cocoa (New York) | 0945-1830 |

1 | 4 |

| Spot, Coffee Arabica | 0915-1830 |

1 | 0.2 |

| Spot, Coffee Robusta | 0900-1730 |

1 | 4 |

| Spot, Copper (High Grade) | 2300-2200 |

1 | 0.3 |

| Spot, Cotton | 0200-1920 |

1 | 0.15 |

| Spot, Gold | 2300-2200 |

0.1 | 3 |

| Spot, Light Crude | 2300-2200 |

0.01 | 2.8 |

| Spot, Natural Gas | 2300-2200 |

0.001 | 3 |

| Spot, Silver | 2300-2200 |

1 | 2 |

| Spot, Sugar (London No. 5) | 0845-1755 |

1 | 0.6 |

| Spot, Sugar (New York No. 11) | 0830-1800 |

0.01 | 3 |

| Commodities, Futures | |||

| Brent Crude, Nov | 0100-2300 |

1 | 10 |

| Brent Crude, Oct | 0100-2300 |

1 | 10 |

| Cocoa (London), Sep | 0930-1650 |

1 | 6 |

| Cocoa (New York), Sep | 0945-1830 |

1 | 10 |

| Coffee Arabica, Sep | 0915-1830 |

1 | 0.6 |

| Copper (High Grade), Sep | 2300-2200 |

1 | 0.6 |

| Gold, Dec | 2300-2200 |

0.1 | 14 |

| Light Crude, Oct | 2300-2200 |

0.01 | 8 |

| Light Crude, Sep | 2300-2200 |

0.01 | 8 |

| London Gas Oil, Aug | 0100-2300 |

1 | 2 |

| Natural Gas, Oct | 2300-2200 |

0.001 | 25 |

| Natural Gas, Sep | 2300-2200 |

0.001 | 25 |

| Platinum, Oct | 2300-2200 |

1 | 6 |

| Silver, Sep | 2300-2200 |

1 | 10 |

| Sugar (London No. 5), Oct | 0845-1755 |

1 | 0.8 |

| Sugar (New York No. 11), Oct | 0830-1800 |

0.01 | 10 |

| Product | Min Stake | Min Stop Distance | G'teed Stop Premium | Min G'teed Stop Distance | |

|---|---|---|---|---|---|

| Commodities, Dailies | |||||

| Spot, Brent Crude | 0.1 | 3 | 2 | 82.14 | |

| Spot, Cocoa (London) | 0.1 | 5 | N/A | N/A | |

| Spot, Cocoa (New York) | 0.1 | 5 | 1 | 5 | |

| Spot, Coffee Arabica | 1 | 0.5 | N/A | N/A | |

| Spot, Coffee Robusta | 0.1 | 0.5 | N/A | N/A | |

| Spot, Copper (High Grade) | 1 | 1 | N/A | N/A | |

| Spot, Cotton | 1 | 0.1 | N/A | N/A | |

| Spot, Gold | 0.02 | 5 | 4 | 404.8 | |

| Spot, Light Crude | 0.1 | 3 | 2 | 77.73 | |

| Spot, Natural Gas | 0.2 | 3 | 4 | 51 | |

| Spot, Silver | 0.1 | 1 | 2.5 | 57.47 | |

| Spot, Sugar (London No. 5) | 1 | 1 | N/A | N/A | |

| Spot, Sugar (New York No. 11) | 0.5 | 1 | N/A | N/A | |

| Commodities, Futures | |||||

| Brent Crude, Nov | 0.5 | 3 | 2 | 80.58 | |

| Brent Crude, Oct | 0.5 | 3 | 2 | 82.92 | |

| Cocoa (London), Sep | 0.1 | 5 | N/A | N/A | |

| Cocoa (New York), Sep | 0.5 | 5 | N/A | N/A | |

| Coffee Arabica, Sep | 10 | 0.5 | N/A | N/A | |

| Copper (High Grade), Sep | 5 | 1 | N/A | N/A | |

| Gold, Dec | 0.2 | 5 | 4 | 410.4 | |

| Light Crude, Oct | 0.5 | 3 | 2 | 76.92 | |

| Light Crude, Sep | 0.5 | 3 | 2 | 78.93 | |

| London Gas Oil, Aug | 5 | 0 | N/A | N/A | |

| Natural Gas, Oct | 0.5 | 3 | 4 | 51 | |

| Natural Gas, Sep | 0.5 | 3 | 4 | 51 | |

| Platinum, Oct | 2 | 1 | N/A | N/A | |

| Silver, Sep | 0.5 | 1 | 2.5 | 57.86 | |

| Sugar (London No. 5), Oct | 1 | 1 | N/A | N/A | |

| Sugar (New York No. 11), Oct | 1 | 1 | N/A | N/A | |

| Product | Contract Months | Last Day of Trading |

|---|---|---|

| Commodities, Dailies | ||

| Spot, Brent Crude | Spot | Rolling |

| Spot, Cocoa (London) | Spot | Rolling |

| Spot, Cocoa (New York) | Spot | Rolling |

| Spot, Coffee Arabica | Spot | Rolling |

| Spot, Coffee Robusta | Spot | Rolling |

| Spot, Copper (High Grade) | Spot | Rolling |

| Spot, Cotton | Spot | Rolling |

| Spot, Gold | Spot | Rolling |

| Spot, Light Crude | Spot | Rolling |

| Spot, Natural Gas | Spot | Rolling |

| Spot, Silver | Spot | Rolling |

| Spot, Sugar (London No. 5) | Spot | Rolling |

| Spot, Sugar (New York No. 11) | Spot | Rolling |

| Commodities, Futures | ||

| Brent Crude, Nov | Monthly | 29/09/2026 00:00:00 |

| Brent Crude, Oct | Monthly | 28/08/2026 00:00:00 |

| Cocoa (London), Sep | Mar, May, Jul, Sep, Dec | 07/09/2026 00:00:00 |

| Cocoa (New York), Sep | Mar, May, Jul, Sep, Dec | 14/08/2026 00:00:00 |

| Coffee Arabica, Sep | Mar, May, Jul, Sep, Dec | 19/08/2026 00:00:00 |

| Copper (High Grade), Sep | Mar, May, Jul, Sep, Dec | 27/08/2026 00:00:00 |

| Gold, Dec | Feb, Apr, Jun, Aug, Dec | 25/11/2026 00:00:00 |

| Light Crude, Oct | Monthly | 22/09/2026 00:00:00 |

| Light Crude, Sep | Monthly | 19/08/2026 00:00:00 |

| London Gas Oil, Aug | Monthly | 10/08/2026 00:00:00 |

| Natural Gas, Oct | Monthly | 25/09/2026 00:00:00 |

| Natural Gas, Sep | Monthly | 26/08/2026 00:00:00 |

| Platinum, Oct | Jan, Apr, Jul, Oct | 25/09/2026 00:00:00 |

| Silver, Sep | Mar, May, Jul, Sep, Dec | 27/08/2026 00:00:00 |

| Sugar (London No. 5), Oct | Mar, May, Aug, Oct, Dec | 10/09/2026 00:00:00 |

| Sugar (New York No. 11), Oct | Mar, May, Jul, Oct | 28/09/2026 00:00:00 |

| Product | Basis of Expiry Price | Daily Funding Premium* | Funding Time | NTR** Multiplier (Pro) | NTR** Multiplier (Retail) |

|---|---|---|---|---|---|

| Commodities, Dailies | |||||

| Spot, Brent Crude | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Cocoa (London) | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Cocoa (New York) | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Coffee Arabica | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Coffee Robusta | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Copper (High Grade) | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Cotton | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Gold | 3.5% | 22:00 | 0.5% | 5.0% | |

| Spot, Light Crude | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Natural Gas | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Silver | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Sugar (London No. 5) | 3.5% | 22:00 | 0.5% | 10.0% | |

| Spot, Sugar (New York No. 11) | 3.5% | 22:00 | 0.5% | 10.0% | |

| Commodities, Futures | |||||

| Brent Crude, Nov | ICE official settlement on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Brent Crude, Oct | ICE official settlement on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Cocoa (London), Sep | ICE official settlement price on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Cocoa (New York), Sep | ICE official settlement on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Coffee Arabica, Sep | ICE official settlement on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Copper (High Grade), Sep | Comex official settlement price on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Gold, Dec | Comex official settlement price on last day of trading +/- spread | N/A | N/A | 0.5% | 5.0% |

| Light Crude, Oct | NYMEX official settlement price on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Light Crude, Sep | NYMEX official settlement price on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| London Gas Oil, Aug | ICE official settlement on last day of trading +/- spread | N/A | N/A | 100.0% | 100.0% |

| Natural Gas, Oct | NYMEX official settlement price on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Natural Gas, Sep | NYMEX official settlement price on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Platinum, Oct | NYMEX official settlement price on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Silver, Sep | Comex official settlement price on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

| Sugar (London No. 5), Oct | N/A | N/A | 1.0% | 10.0% | |

| Sugar (New York No. 11), Oct | ICE official settlement on last day of trading +/- spread | N/A | N/A | 0.5% | 10.0% |

^Please note that all markets close at 22:00 on a Friday and reopen from 22:00 on a Sunday as specified per individual market trading hours.

†Please note that to see specific expiry dates for certain markets, you need to log in to your account and then click on the 'i' button next to your chosen market. The specific expiry date for that product will be shown on the market information ticket.

*These products are continuously rolled overnight. For funding calculations see the Financial FAQs section for more.

**NTR relates to Notional Trading Requirement (aka 'Initial Margin' and 'Deposit') and refers to the funds required as initial outlay for a trade. It is not the total amount that can be lost on the trade but the minimum amount you need to set aside to place a specific trade. NTRs vary from product to product, please see our Market Information Sheets above for specific details.

*** Spreads are subject to variation, especially in volatile market conditions. Our spreads will change during different times of the day and different market conditions to reflect the available liquidity in the underlying market that our price is based on. Larger trades may be subject to wider spreads, more information on this is displayed on the information button alongside each market on our platform.

find out more on

Spot Gold and Spot Silver Funding

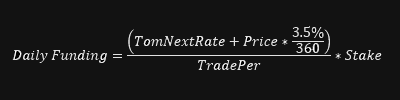

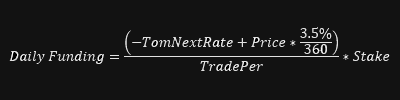

Our funding rate for Spot Gold and Spot Silver consists of two parts: the Tom-Next rate for that market and an admin fee (3.5% annualised). The charge is applied at 10pm every weekday.

The formula describes the charge, so a positive number means you’re debited (pay funds) and a negative number means you’re credited (receive funds).

For long positions:

You pay the Tom-Next rate therefore it is added to the charge.

For short positions:

You receive the Tom-Next rate therefore it is subtracted from the charge (treat stake as a positive number).

TradePer = What we define 1 point to mean in terms of the visible price, this can be found in the Market Information section next to the displayed price on the platform.

Stake = Account currency unit per point.

Price = Price of commodity at 10pm

TomNextRate = Overnight fee/credit to keep your position open without settling.

The formula can be broken down to essentially two components. One is the TomNextRate component which is found by multiplying the rate by the stake and scaling it by TraderPer to convert to points. The second component is the Spreadex admin fee which is found by multiplying the notional of the position (stake*(price/TradePer)) by the daily admin fee (hence the division by 360).

For example, suppose we have the following situation:

|

Position |

Long £1/pt Spot Gold |

|

Price of Spot Gold at 10pm |

1810 |

|

TradePer |

0.1 |

|

Gold Tom-Next rate at 10pm |

0.237 |

Your daily funding charge breakdown would be:

Tom-Next component = (0.237 /0.1) * 1 = £2.37

Admin fee = [(1810*0.035/360)/0.1] *1 = £1.76

Total Funding Charge = £2.37 + £1.76 = £4.13

Note, here, you are paying (account debit) the Tom Next rate, if your position was the opposing direction you would receive (account credit) the Tom Next rate, in either case you would always pay the Spreadex admin charge. Also note that on a Wednesday, the Tom-Next component is multiplied by 3 and one day of admin fee applies. On a Friday, one day of Tom-Next applies and the Spreadex admin fee component is multiplied by 3. (See below for more details)

Find out more on

Key concepts regarding gold/silver funding

Spot Gold and Silver prices come from various liquidity providers, including banks and market makers. These providers base their quotes on real-time supply and demand in the precious-metals market. Supply and demand can shift for many reasons, such as jewellery demand, their role as safe-haven assets, changes in interest rates, which in turn influence the prices you see.

On Wednesdays, we apply triple Tom-Next funding for Spot Gold and Silver. This reflects the underlying market's T+2 settlement convention, where positions held through Wednesday roll settlement over the weekend. As a result, if you hold a position past 10pm Wednesday, the applicable three-day Tom-Next funding adjustment will apply.

Around bank holidays, the number of days applied to the Tom-Next charge may differ. This is because the Tom-Next rate reflects the actual number of non-settlement days being rolled over, which increases when a bank holiday falls within the settlement window. For example, if Monday is a bank holiday, the Wednesday Tom-Next charge may be 4x rather than 3x.

The Spreadex admin charge is applied separately. For positions held over the weekend, this charge is applied at 3x on Friday.

Please see above for an example of how the daily funding amount is calculated.

find out more on

SPot energies and spot softs funding

If you hold a spot energy or spot soft commodity position through 10pm (UK time) on a weekday, a funding adjustment will be applied to your account. This adjustment has two components:

- Daily basis adjustment — reflects the daily movement of the spot price along the futures curve. This is not a separate charge. It is a market adjustment that is typically offset by the corresponding movement in the spot price. It can be a debit or a credit depending on the direction of your trade and the relationship between the two underlying futures contracts.

- Admin fee (3.5% annualised) — applied daily, this is the cost of holding your position overnight. It is always a debit, regardless of the direction of your trade.

On Fridays, the funding adjustment covers three days (Friday, Saturday and Sunday), so both components will be three times the usual daily amount.

The formulas below are shown for transparency — you don't need to calculate this yourself. A positive result means you are debited (pay funds). A negative result means you are credited (receive funds).

If long:

Daily Funding Rate = Daily Basis Adjustment + Admin Fee Rate

If short:

Daily Funding Rate = Admin Fee Rate − Daily Basis Adjustment

Your funding charge or credit = Daily Funding Rate × Stake

Where:

Daily Basis Adjustment = (Next Future Price − Front Future Price) / (TradePer × Days Between Contracts)

- Front Future Price = price of the nearest futures contract at 10pm

- Next Future Price = price of the following futures contract at 10pm

- TradePer = what we define 1 point to mean in terms of the visible price (shown in the Market Information section on the platform)

- Days Between Contracts = the number of days over which the price transitions from one contract to the next (i.e. the number of days between successive contract expiries)

Admin Fee Rate = (Spot Mid Price × 0.035) / (TradePer × Days in Year)

- Spot Mid Price = closing mid-price of the spot market at 10pm

- Days in Year = 360

Worked example

Suppose it is 30/03 and you hold a short position of £2/pt in Spot Brent Crude. At 10pm the market looks like this:

|

Spot Brent Crude price |

8240 |

|

TradePer |

1 |

|

Brent Crude, May — front contract |

8236 |

|

Brent Crude, June — next contract |

8207 |

|

Previous contract expiry |

27/02 |

|

Front contract expiry |

30/03 |

Step 1 — Daily Basis Adjustment:

Days Between Contracts = 30/03 − 27/02 = 32 days

Daily Basis Adjustment = (8207 − 8236) / (1 × 32) = −0.90625

The result is negative because the next contract is priced lower than the front contract. For a short position, a negative basis adjustment results in a debit (the formula subtracts a negative, making it a positive charge).

Step 2 — Admin Fee Rate:

Admin Fee Rate = (8240 × 0.035) / (1 × 360) = 0.801

Step 3 — Apply the short formula:

Daily Funding Rate = 0.801 − (−0.90625) = 1.70725

Daily Funding Charge = 1.70725 × £2 = £3.41 debit

Breakdown:

|

Component |

Rate |

Amount (× £2 stake) |

What it means |

|

Daily basis adjustment |

−0.90625 |

£1.81 debit |

Offset by the downward drift in the spot price |

|

Admin fee |

0.801 |

£1.60 debit |

Your actual cost for holding overnight |

|

Total |

1.70725 |

£3.41 debit |

In this example, the front contract (8236) is priced higher than the next contract (8207), so the spot price drifts lower each day. As a short position holder, you benefit from this downward drift in the spot price. The £1.81 basis adjustment debit offsets that corresponding price movement. The actual cost of holding this position overnight is the admin fee of £1.60.

Find out more on

DAILY BASIS ADJUSTMENTS

The prices of our spot energy and spot soft commodity markets are derived from the two nearest futures contracts on the underlying asset, as these tend to offer the most liquidity. Our spot price is a weighted average of these two contracts: as the front contract approaches expiry, its influence on the spot price gradually decreases and the next contract's influence gradually increases. This creates a smooth transition between contracts rather than a sudden price jump. However, it also means the spot price moves slightly each day as part of this transition — even if the underlying market is otherwise unchanged.

The daily basis adjustment reflects this gradual price movement. It is applied to your account to offset the corresponding movement in the spot price, similar to how a dividend adjustment works on an index. It is not a separate charge or fee.

When the front contract is priced higher than the next contract, the spot price drifts lower each day as it transitions towards the lower-priced contract. In this case long positions see a loss from the downward price drift but receive a basis adjustment credit to offset it, while short positions see a gain from the downward price drift but pay a basis adjustment debit to offset it.

When the next contract is priced higher than the front contract, the spot price drifts higher each day. In this case long positions see a gain from the upward price drift but pay a basis adjustment debit to offset it, while short positions see a loss from the upward price drift but receive a basis adjustment credit to offset it.

In both scenarios, the basis adjustment and the spot price movement are typically offsetting.

The size of the daily basis adjustment depends on the price difference between the two futures contracts. When market conditions cause a large difference between these contracts — for example during periods of supply disruption or heightened uncertainty — the basis adjustment will also be larger, and the funding entry on your ledger may appear high. However, the larger the basis adjustment, the larger the corresponding spot price movement that offsets it. The admin fee (3.5% annualised) is the cost of holding your position overnight.

For a fuller explanation of why the funding entry on your account can sometimes appear larger than expected, see our page on Understanding Overnight Funding on Spot Energies.

find out more on

Tomorrow-Next (Tom-Next) Rates

The Tom-Next rate for a given market is the rate you must pay to roll a position (i.e. stop your position being closed tomorrow and keep it open until the next day). We utilise it in some of our funding charge formulas. The rate itself is determined by banks and the market.

For example, if you buy Spot Gold in the official markets (rather than just placing a bet on its price like you do with us), then this trade will usually settle T+2, meaning that (loosely speaking) two working days after the trade date, you will be locked into having gold delivered.

Suppose you bought Spot Gold on Monday, and it’s now Tuesday. As it stands, you have gold being delivered tomorrow (Wednesday), but if you don’t want to take this delivery tomorrow and would rather keep the position open, then you can roll it at whatever the prevailing Tom-Next rate is. From the perspective that it is now Tuesday, rolling the position once via Tom-Next rates extends the settlement date by one day to Thursday.

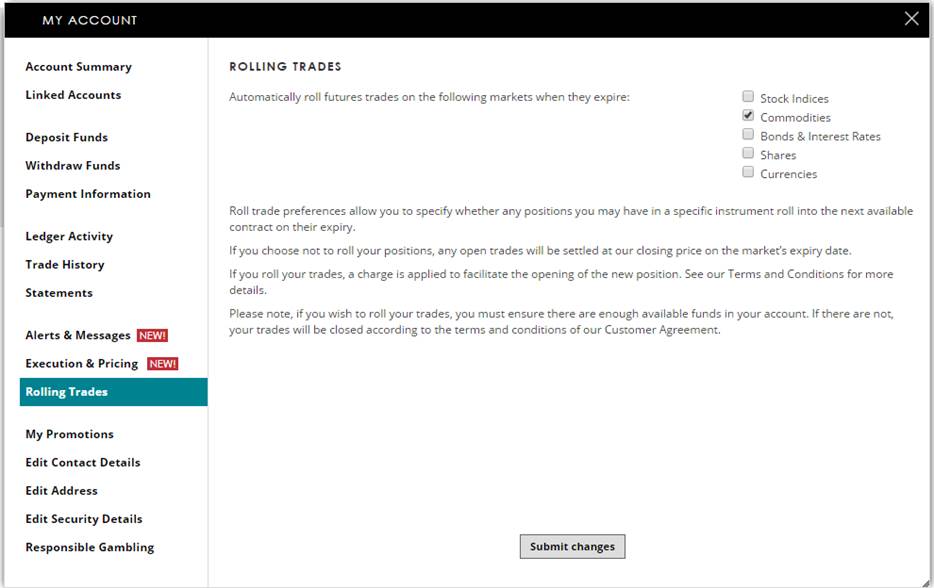

HOW TO

roll a COMMODITY trade

All spot commodity trades will automatically remain open indefinitely. Futures trades will close at the expiry date of the contract. You can specify whether you would like to roll any commodity futures trades to roll into the next contract by visiting the Rolling Trades page within My Account once you have logged in. Click the following link to find out information on setting your Trading Preferences. You can find the expiry date of each futures contract on the information button on our platform.

When you first open the account, as a default setting, all preferences are set for trades not to roll. If you wish for your trades to roll past their respective expiry dates it is essential that you have updated these preferences.

If you would like to roll all commodity trades, please ensure that the ‘Commodities’ box is ticked, as shown in the above example

Any stops or limits you have attached to your trade will be rolled over also, they will be adjusted to reflect the price of the new contract you have been rolled into.

how to

go long and short in the same market

You are able to open a trade in the opposing direction to an existing trade in the same market, this is called a forced open trade. Rather than your positions netting off, you would now have open positions both long and short.

Forced open trades can be opened by placing a trade at the live available price or alternatively by adding an order to open at a different price, should the price subsequently move to the level of your order your forced open trade will be opened.

Forced open trades can be executed by ticking the forced open position on the deal ticket, you can also update your settings so the default setting is for forced open to always be selected.

It is important to note that placing forced open trades will result in increased costs. If you have forced open positions open overnight, the funding adjustments will be applied to all positions open and will lead to increased funding costs. These costs can be avoided by not placing forced open trades and just allowing your positions to net off eg. £10 long position and £10 short position = no net overall exposure.

how to work out the

NTR/Margin for a commodities trade

The Notional Trading Requirement (NTR, Initial Margin or Margin) is the amount of money we require for you to open a trade in a specified product. The NTR will normally be displayed as a percentage and can be found in the Commodities market information pages.

For example, placing a £10 trade on Silver at 5200 would require £5200 of NTR, as the NTR rate is 10% (£10 x 5200 x 10%).

The majority of markets will have a larger NTR rate for larger stake sizes. This is to reflect the increased risk of larger positions, we require a greater deposit the bigger the position size. The NTR tiers can be found on the information button alongside each market on our platform. The NTR tiers don't act as a cliff edge, they act as a step system where the NTR margin rate for each tier is applied against your position.

For example, if Silver has tiered margin catergories of 10% up to a stake of £500 and 20% above £500 and your stake was £505, only £5 of your position would be margined at 20%.

If you have a ‘Force Open’ position or an opposing trade in both the futures and daily you will only be charged NTR on the trade with the larger stake.

find out more on

Gold

Gold has always been a symbol of wealth due to its look and rarity and is by far the most popular of the precious metals when it comes to investment, trading or financial spread betting.

Gold futures are primarily traded on the New York Commodities Exchange (COMEX), a subsidiary of the CME Group (Chicago Mercantile Exchange). Its price is quoted in US dollars per ounce.

Gold is renowned for holding its value and is regarded as a safe haven for investors to turn towards to diversify their portfolio and offer protection during times of economic uncertainty.

find out more on

silver

Silver had been regarded as a form of money and a store of value for more than 4,000 years until the end of the silver standard in 1971 when the metal lost its role as legal tender in the United States.

Now silver is still commonly used as a form of investment, although is not anywhere near as popular as gold in this regard. It is also used in industrial applications such as in conductors. Silver futures are primarily traded on the New York Commodities Exchange (COMEX), a subsidiary of the CME Group (Chicago Mercantile Exchange), and its price is quoted in cents per troy ounce.

In a similar manner to gold, silver is seen as a commodity to turn to during times of economic uncertainty. While silver often tracks gold prices, it can often be much more volatile.

find out more on

Light crude

Oil is one of the world’s most critical and valuable natural resources, with the price of the commodity affecting consumers every day by influencing the cost of certain goods and affecting heating, petrol or gasoline prices.

Crude oil is the world’s most actively traded commodity and the two most heavily traded contracts on crude oil are the Brent Crude Oil contract and the West Texas Intermediate (WTI) Light Sweet Crude Oil contract.

WTI Light Crude oil is crude oil of a very high quality, mainly refined in the Midwest and Gulf Coast region of the United States. It is considered the major benchmark of crude oil in the Americas.

Futures contracts of WTI Crude Oil are traded on both the InterContinental Exchange (ICE) and New York Mercantile Exchange (NYMEX) and in Dubai by the Dubai Gold and Commodities Exchange. Light Crude futures are traded in units of 1,000 US barrels (42,000 gallons) with prices quoted in US dollars.

find out more on

brent crude

Crude oil is the world’s most actively traded commodity and the two most heavily traded contracts on crude oil are the Brent Crude Oil contract and the West Texas Intermediate (WTI) Light Sweet Crude Oil contract.

Brent Crude, or Brent blend, is a combination of oil from 15 different fields in the Brent and Ninian systems in the North Sea. Although it could be said the oil is ‘light’ and ‘sweet’, it is not thought of as ‘light’ or as ‘sweet’ as West Texas Intermediate. It is ideal for making gasoline and middle distillates, both consumed in large quantities in Northwest Europe.

Brent Crude gets its name from the naming policy of operating companies, which originally named its fields after birds and in particular the Brent Goose. Brent Crude is generally considered as the major benchmark for other crude oils in Europe or Africa and prices for other crude oils are often based on a differential to Brent.

Until 1995 the commodity was traded on the International Petroleum Exchange in London, but are now traded on the electronic Atlanta-based Intercontinental Exchange Inc. (ICE), previously known as the Board of Trade of the City of New York (NYBOT).

find out more on

copper

Copper is a primary industrial metal used mainly in construction. Just like gold and silver, copper can also be traded on the financial markets with futures prices often considered an accurate barometer of economic growth.

Copper futures are primarily traded on the New York Commodities Exchange (COMEX), a subsidiary of the CME Group (Chicago Mercantile Exchange), and its price is quoted in US cents per pound. Although not as heavily traded or as valued as gold, copper is 100% recyclable and has hit close to record highs in recent years making it a target for theft either from underground communication cables or derelict buildings.

Find out more on

Palladium

Palladium and platinum are the most widely used of the six platinum group metals, which also include rhodium, ruthenium, osmium and iridium. They are used in manufacturing processes in a range of industries due to their catalytic functions, conductivity and resistance to corrosion.

Palladium is often found in catalytic converters as it helps lessen the impact of certain gases on the environment and is found extensively within computers and televisions. In the future, palladium will play a key role within hydrogen fuel cells.

Palladium futures are primarily traded on the New York Commodities Exchange (COMEX), a subsidiary of the CME Group (Chicago Mercantile Exchange), and its price is quoted in US dollars per troy ounce.

find out more on

Platinum

Platinum and palladium are the most widely used of the six platinum group metals, which also include rhodium, ruthenium, osmium and iridium. They are used in manufacturing processes in a range of industries due to their catalytic functions, conductivity and resistance to corrosion.

Platinum has more industrial uses than gold and silver combined and is also used in jewellery – where it is known as white gold – because of its resistance to wear and tarnishing.

Platinum futures are primarily traded on the New York Commodities Exchange (COMEX), a subsidiary of the CME Group (Chicago Mercantile Exchange), and its price is quoted in US dollars per troy ounce.

Find out more on

Natural gas

Natural gas is known as a very clean fuel which is used extensively around the world. A bulk of natural gas is in Russia and in the Middle East. It is predominately used in energy production.

Natural Gas futures are traded primarily on the New York Mercantile Exchange (NYMEX), a subsidiary of the CME Group (Chicago Mercantile Exchange), with prices quoted in US dollars per million British thermal units.

find out more on

cocoa

Cocoa is used in a variety of culinary applications and is derived from the cacao tree. Much of cocoa comes from West Africa and part from South America, where it was even once used as a form of currency.

Cocoa is the world’s smallest soft commodity market and is traded predominantly on the InterContinentalExchange (ICE). Cocoa prices are quoted in US dollars per metric ton.

When spread betting on cocoa you trade per dollar movement. Price movements can sometimes be volatile with up to 100 point movements per day occurring with regularity.

When spread betting on cocoa it is worth considering several major influences on the price such as the prevalence of disease, which can destroy cocoa crops, political instability in cocoa growing countries within West Africa or South America and the demand of cocoa by other countries around the world.

As cocoa’s price is quoted in US dollars, any fluctuations in the value of the American currency can also influence the price of cocoa.

find ouT more on

corn

Corn is used primarily to feed livestock, but also has other uses in food production, bio fuels and even within commercial applications such as glue. The United States produces more than 50% of the world’s total harvest as the majority of the crops in the United States are genetically modified.

Corn futures are primarily traded on the Chicago Board of Trade (CBOT), a subsidiary of the CME Group (Chicago Mercantile Exchange), with prices quoted in cents per bushel.

When spread betting on corn you trade per cent movement. Price movements can sometimes be volatile with up to 100 point movements per day occurring with regularity.

When spread betting on corn it’s worth considering several major factors which can influence the price. The demand for corn comes mainly from livestock feed and bio fuel production so it is important to monitor the demand within these markets. It is important to monitor weather, disease and other factors which could reduce or improve the size of the harvest. As corn’s price is quoted in US dollars, any fluctuations in the value of the American currency can also influence the price of corn.

find out more on

soyabeans

Soyabeans are used as protein feed for livestock, as a meat-alternative and in other products such oils. The US is a major producer of soyabeans, along with Brazil and Argentina.

Soyabean futures are primarily traded on the Chicago Board of Trade (CBOT), a subsidiary of the CME Group (Chicago Mercantile Exchange), with prices quoted in cents per bushel.

When spread betting on soyabeans take care to consider several major influences which can affect the price. Disease such as soyabean rust can damage crops, and weather can have major consequences on the size of the crops. Demand in the future may be spurned further by an increasing reliance on bio fuels, such as that produced from the soyabean. As soyabean’s price is quoted in US dollars, any fluctuations in the value of the American currency can also influence the price of soyabeans.

find out more on

sugar

Sugar is used as a natural sweetener for food and drinks and increasingly used to produce ethanol, a biofuel. Sugar can be produced from sugar beet or sugar cane. Most production comes from Brazil, the United States and China.

Sugar #11 futures are primarily traded on the InterContinentalExchange (ICE) with prices quoted in cents per pound.

When spread betting on sugar there are several major factors to monitor which can influence the price. These would include the demand for alternatives to sugar such as artificial sweeteners, the demand for bio fuel, which is inversely correlated to the price of crude oil, and political influences such as subsidies. As sugar’s price is quoted in US dollars, any fluctuations in the value of the American currency can also influence the price of sugar.

find out more on

wheat

Wheat is used in a variety of ways to produce livestock feed and various different foodstuffs from biscuits to flour. It is also used to distil alcohol. The biggest wheat producer is China, but Russia, Canada and the US produce sizable amounts.

Wheat futures are primarily traded on the Chicago Board of Trade (CBOT), a subsidiary of the CME Group (Chicago Mercantile Exchange), with prices quoted in cents per bushel.

When spread betting on wheat there are several major influences to consider which may affect the price. These would include the demand for biofuels, the availability and price of substitute products (especially when it comes to livestock pricing) and any diseases which could damage crops. As wheat’s price is quoted in US dollars, any fluctuations in the value of the American currency can also influence the price of wheat.